Waiting On The Evidence

Our cyclical weight of the evidence suggests equity market risks outweigh opportunity and caution remains warranted

The new year can bring the hope of a better market environment. While it can be tempting to draw conclusions about all of 2023 from how December closed and January has begun, we would counsel patience. One lesson from 2022 is that normally reliable indicators of strength can be distorted in elevated volatility environments. The evidence has not improved and caution remains warranted. The liquidity environment remains poor, last year’s pattern of lower lows and lower highs is intact and the trend in the net new high data has been slow to turn.

Liquidity: Money supply is contracting and liquidity is evaporating as virtually all global central banks are in tightening mode. Historically it has not paid to fight the Fed (and its friends).

Economic Fundamentals: What began as weakness in housing and new orders is continuing to expand. The 6-month change in the leading economic index is at a level not typically seen outside of recession.

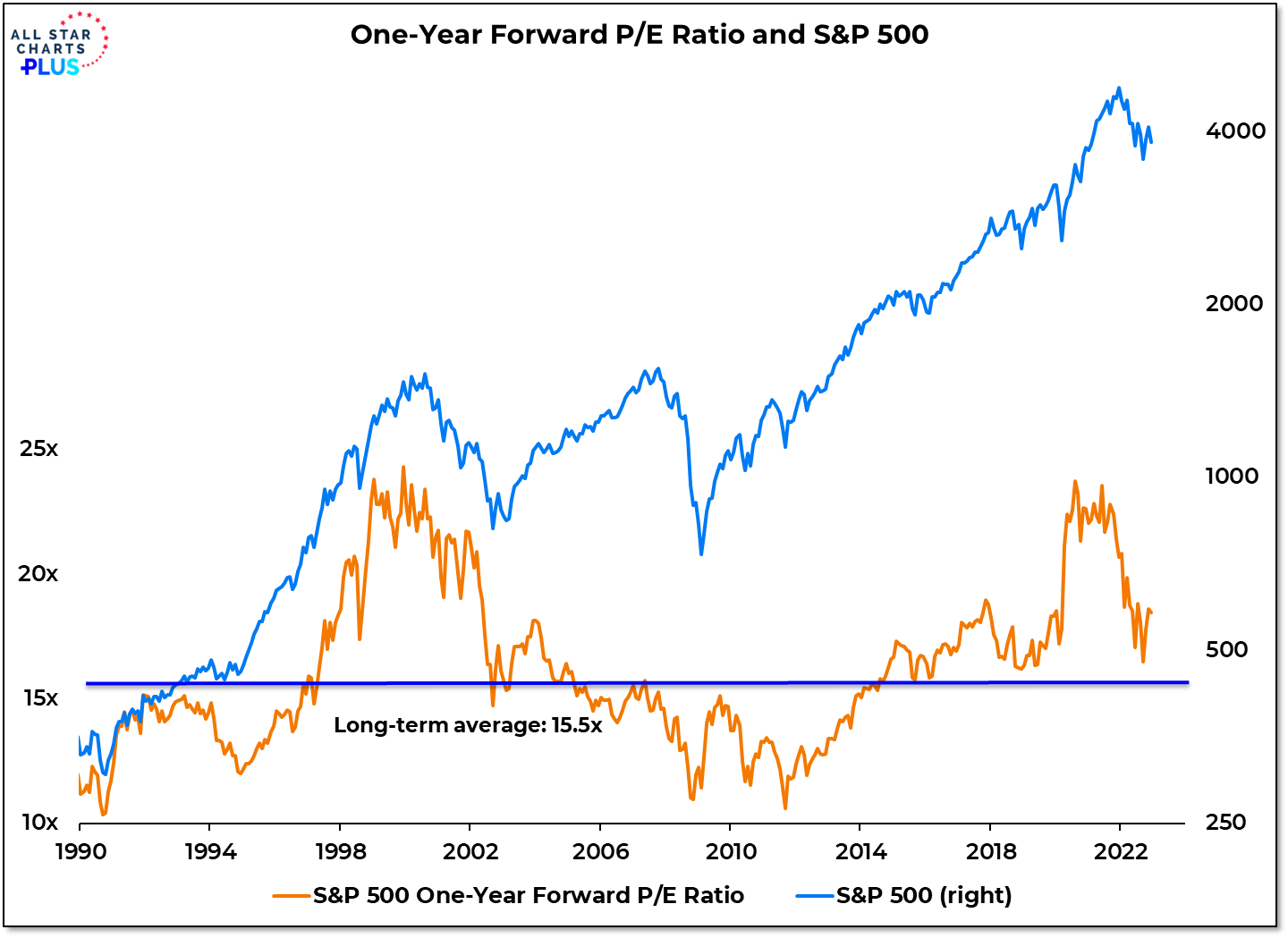

Valuations: Even after last year’s price decline, stock market valuations remain elevated.

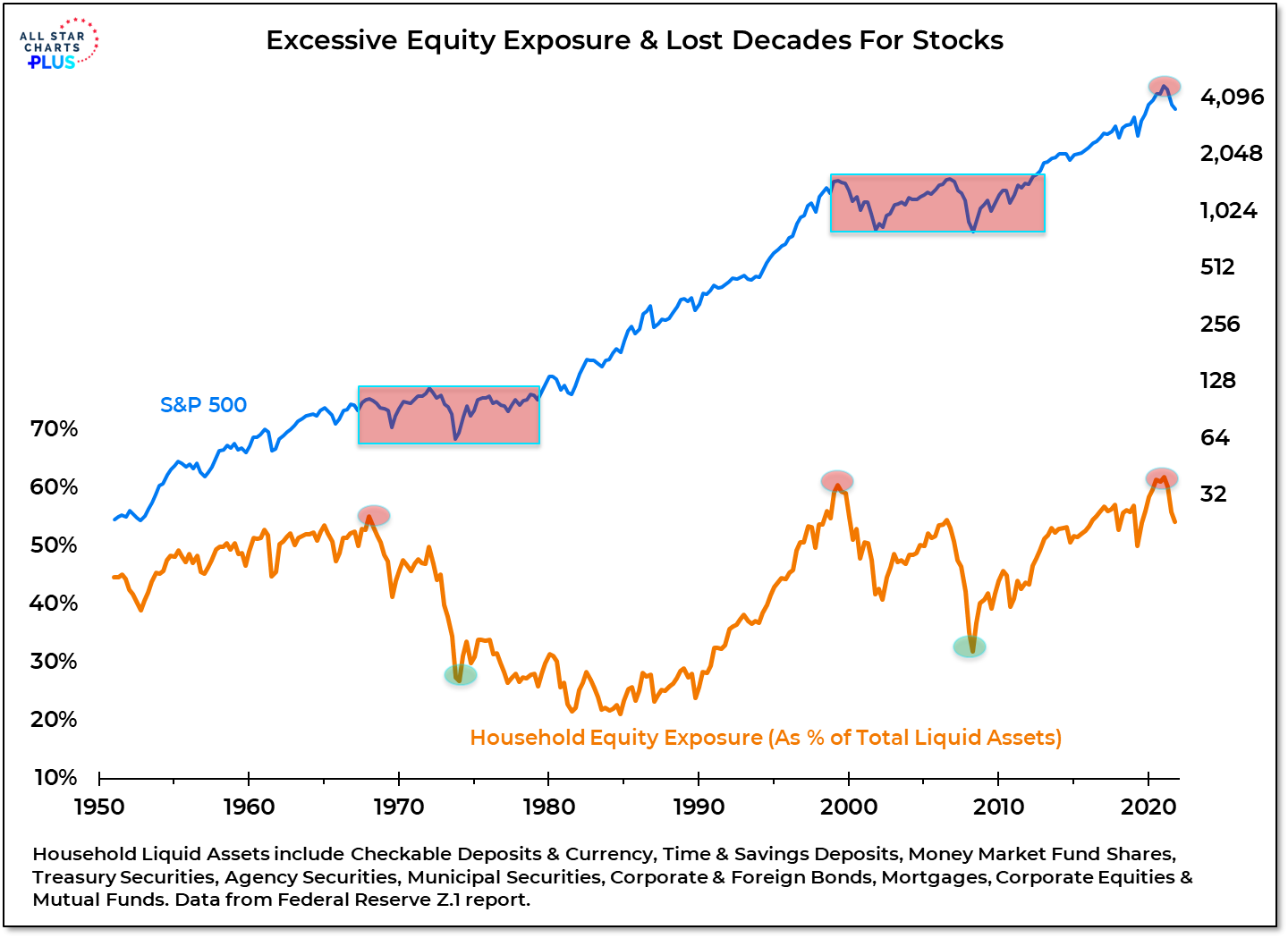

Sentiment: Looking past what investors are saying and focusing on how they are positioned, we see that household equity remains elevated and is similar to what was seen as stocks entered past secular bear markets.

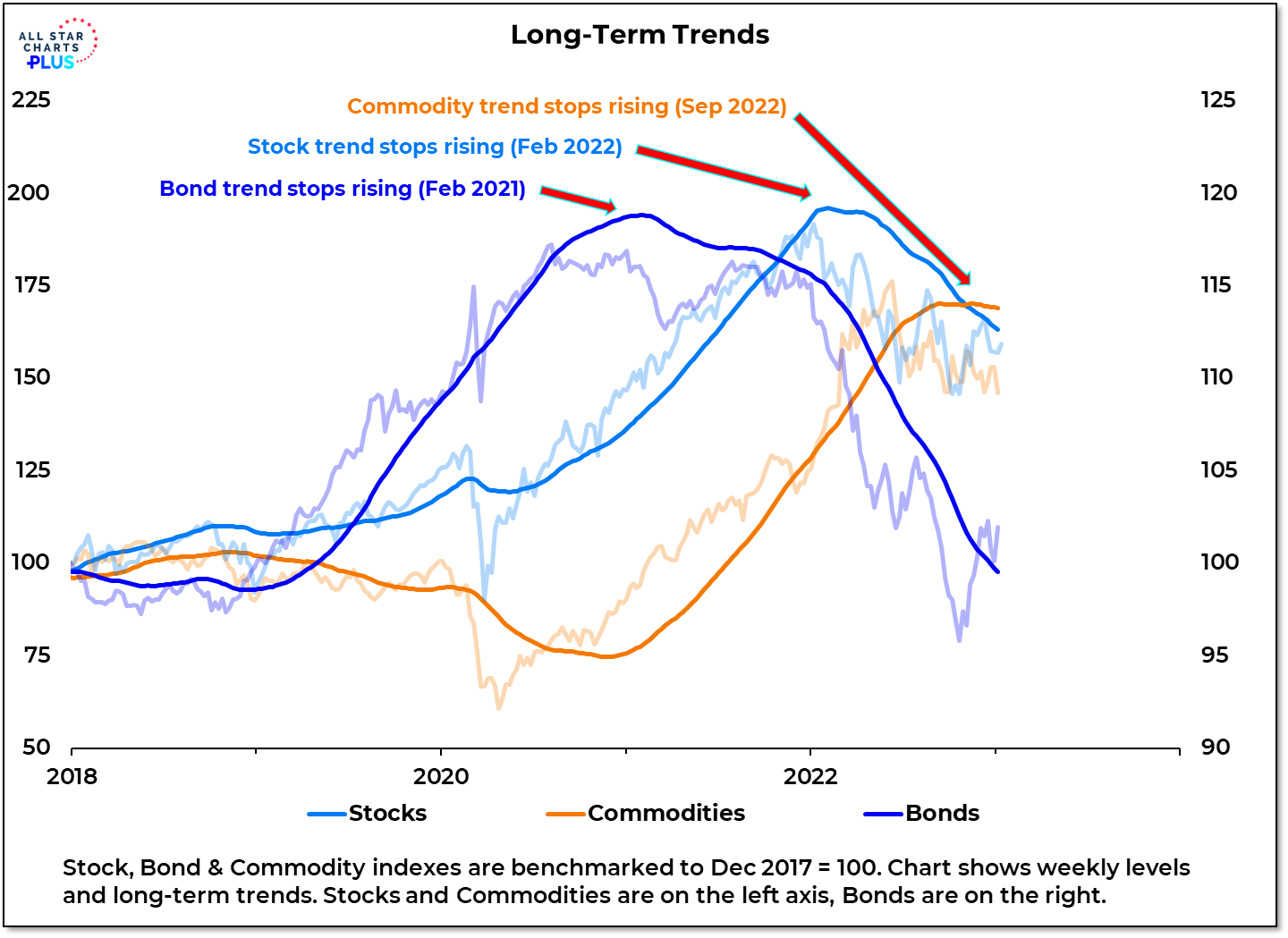

Market Trends & Momentum: Seasonals are a tailwind, but the S&P 500 continues to make lower highs and lower lows. The downtrends in bonds, stocks and commodities that emerged over the past two years are intact.

Breadth: The market in 2022 experienced an unprecedented combination of market weakness and volatility. Bull markets are characterized by new highs exceeding new lows on a consistent basis and that has yet to happen in this cycle.