Trendlines over Headlines: Weighing the Evidence

Discussing challenging trends, sentiment vs positioning and silver lining for stocks as investors face a paradigm shifting environment

On Thursday, I got together with my friend Patrick Dunuwila of The Chart Report to talk through the evidence of opportunity and risk in the market as we begin Q2.

You can watch the entire video here:

We covered a lot, here are some of my favorite charts from the conversation:

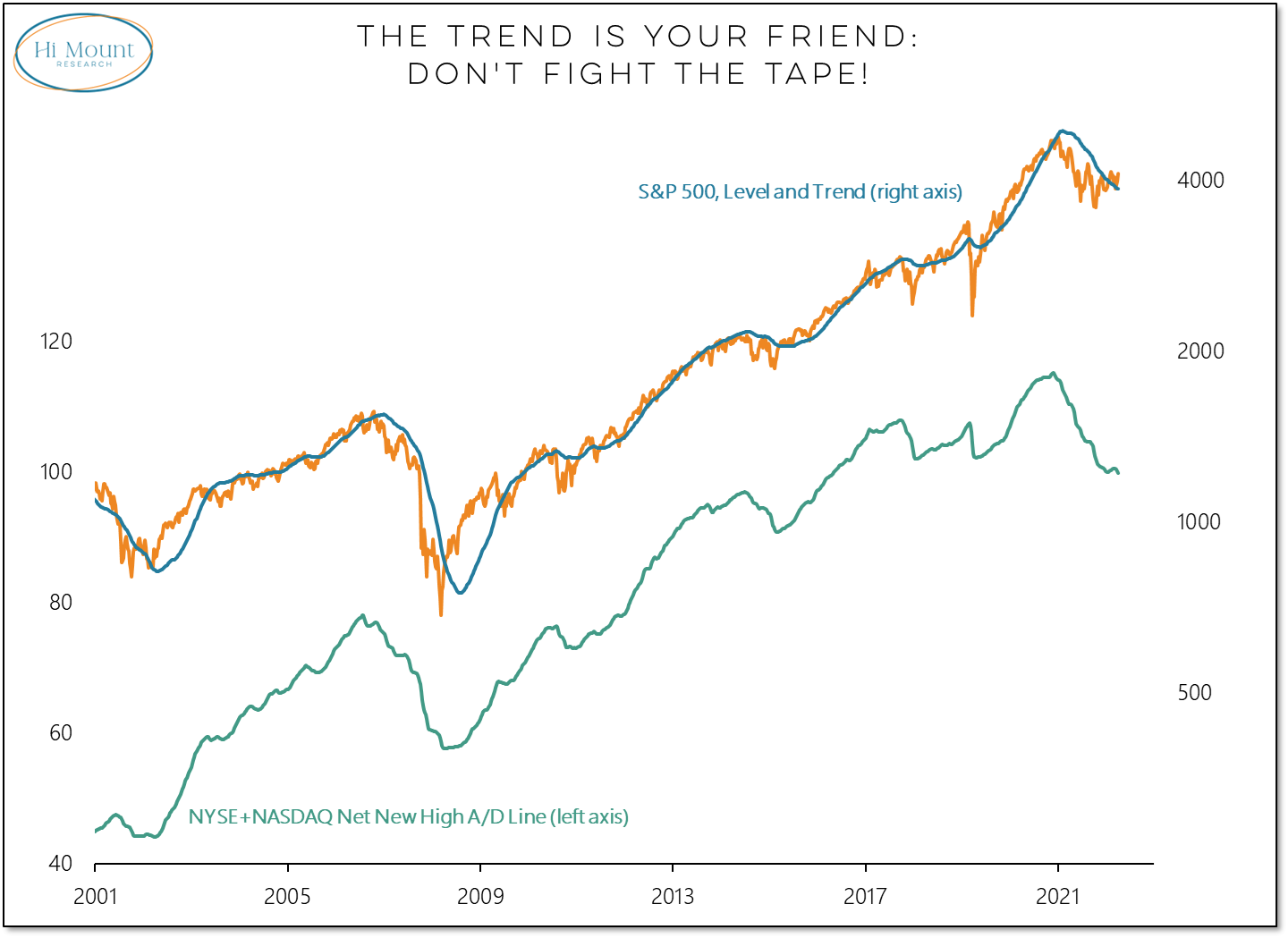

As we began Q2, our breadth and trend indicators were not showing evidence of bull market behavior.

If you're looking for market rallies to be sustained while more stocks are making new lows than new highs (which is currently the case), you’re fighting the tape.

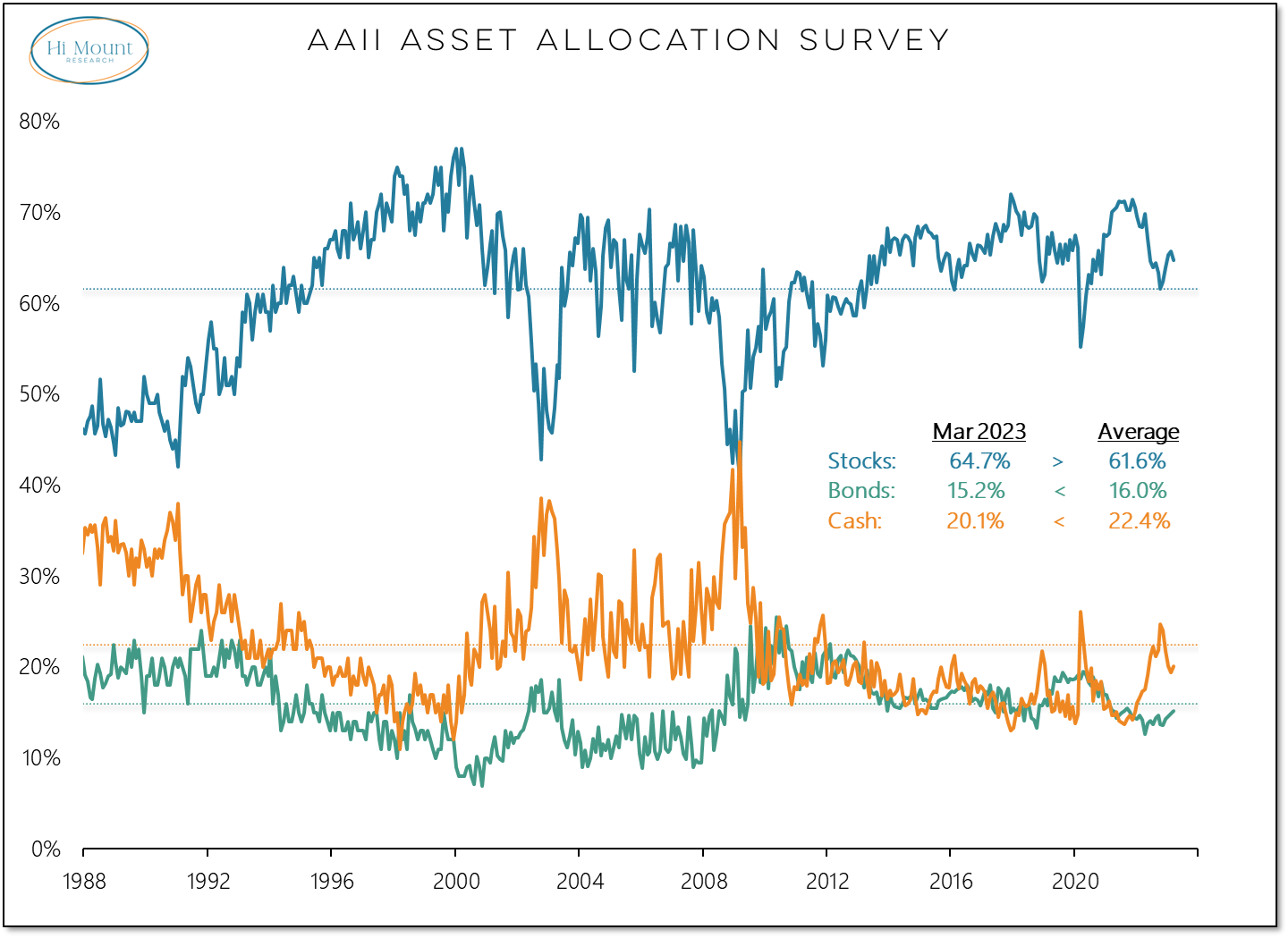

Pessimism has been persistent over the past year, but investors have not abandoned equities. Forward returns for stocks are low when equity exposure has been elevated. Price weakness has done little to unwind excessive investor positioning.

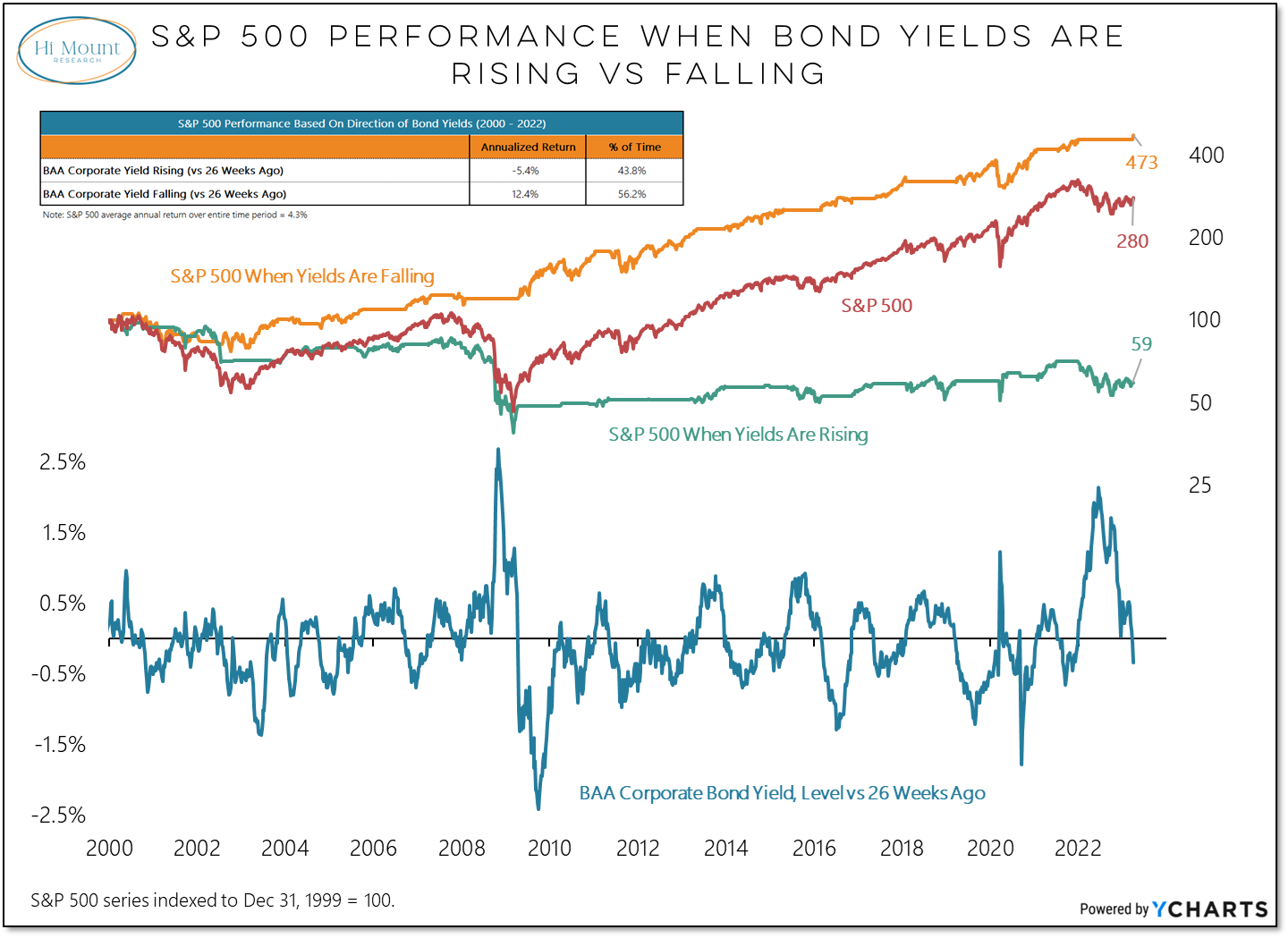

Corporate bond yields are lower now than 26 weeks ago. We can put arguments whether the Fed has gone to far or whether the bond market is right to be fighting the Fed on the shelf and just focus on this relationship. All the net gains in the S&P 500 over the past 2+ decades have come when corporate bond yields have been falling.

The past decade was dominated by US leadership. Now, the rest of the world is taking the lead. The home-country bias that was a tailwind for US investors over the past decade could be a headwind in the next decade.

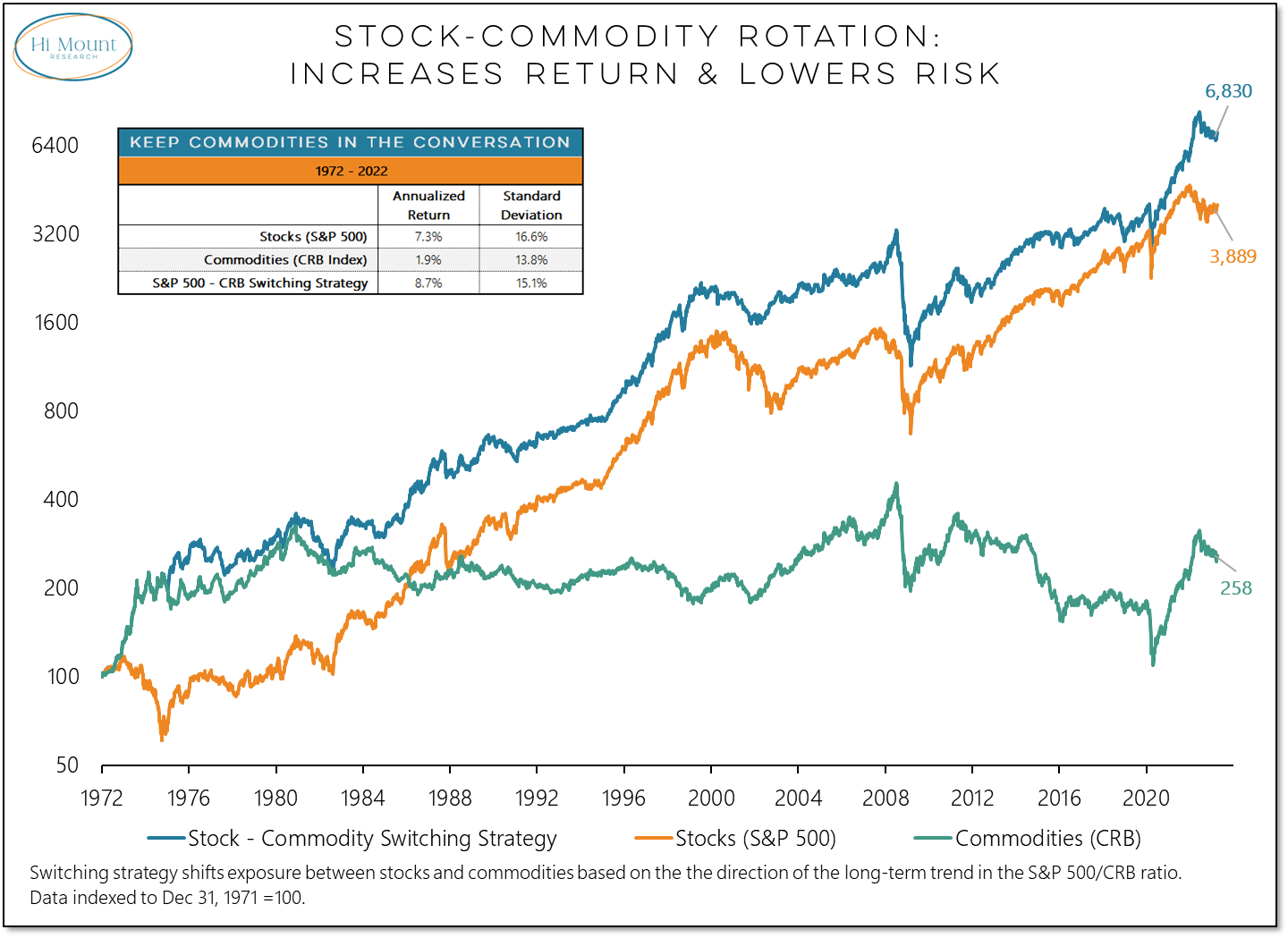

The leadership from commodities over the past two years was also a new phenomenon for investors whose perspective is limited to the past decade.

While the trend is back to favoring stocks over commodities, investors benefit when they don’t take commodities out of the conversation just because they are out of the current asset allocation mix. Following the relative leadership between stocks and commodities leads to better outcomes for investors.