Lackluster Participation Doesn't Keep Indexes From Hitting New Highs

A rally fueled by improving expectations lacks broad support

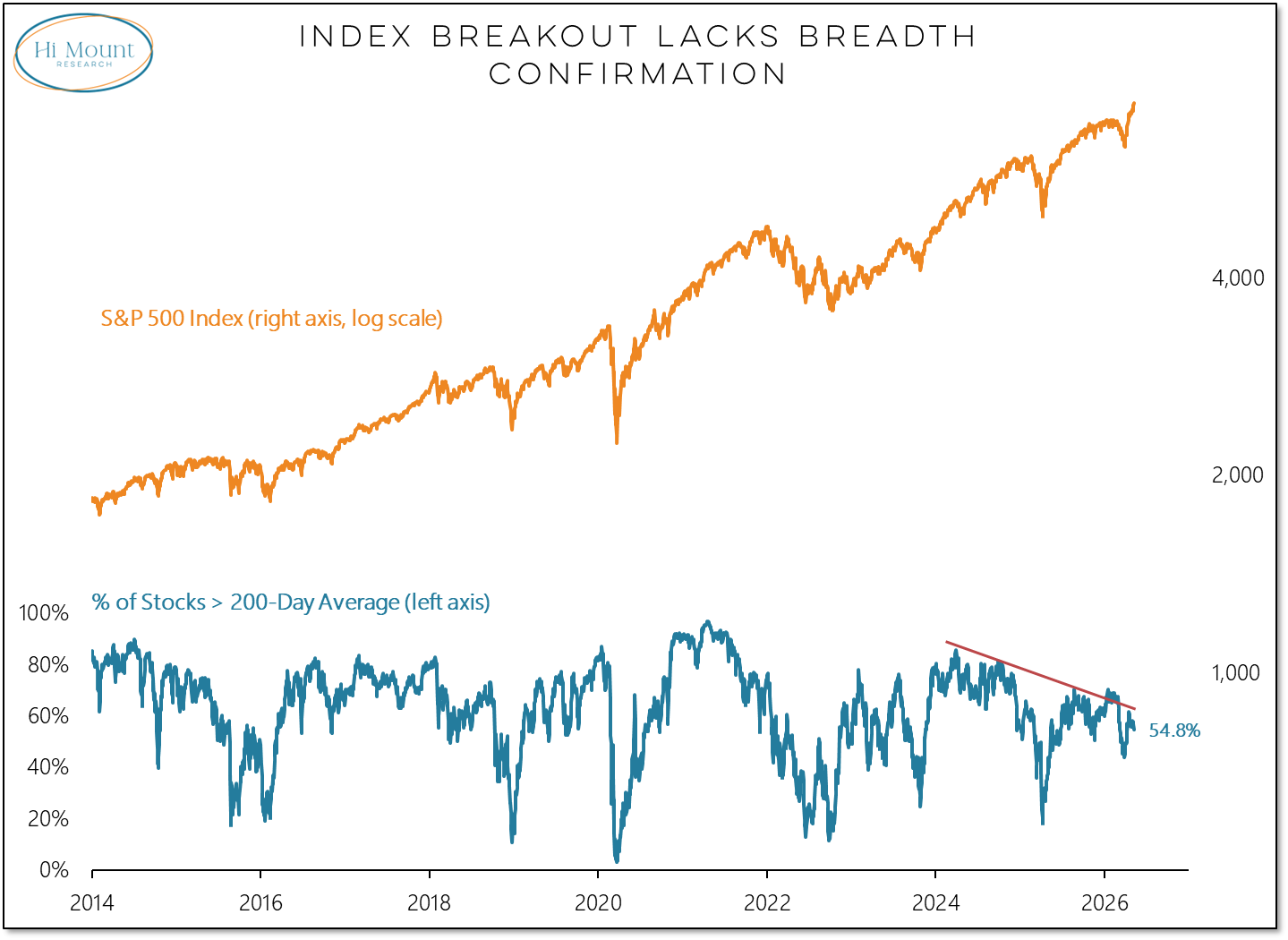

The indexes are hitting new highs. The S&P 500 is up 6 weeks in a row and finished last week just shy of 7400. The NASDAQ composite, which is also up 6 weeks in a row, pushed 4.5% further into record territory last week.

Beneath the surface, however, the picture is not as rosy. The index is hitting record levels and yet only slightly more than half of the constituents in the index are even above the long-term moving average - for the median stock in the index, a new 52-week high would require a rally of more than 15%. The percentage of stocks above their 200-day average is falling and by the end of last week it dropped below 55%.

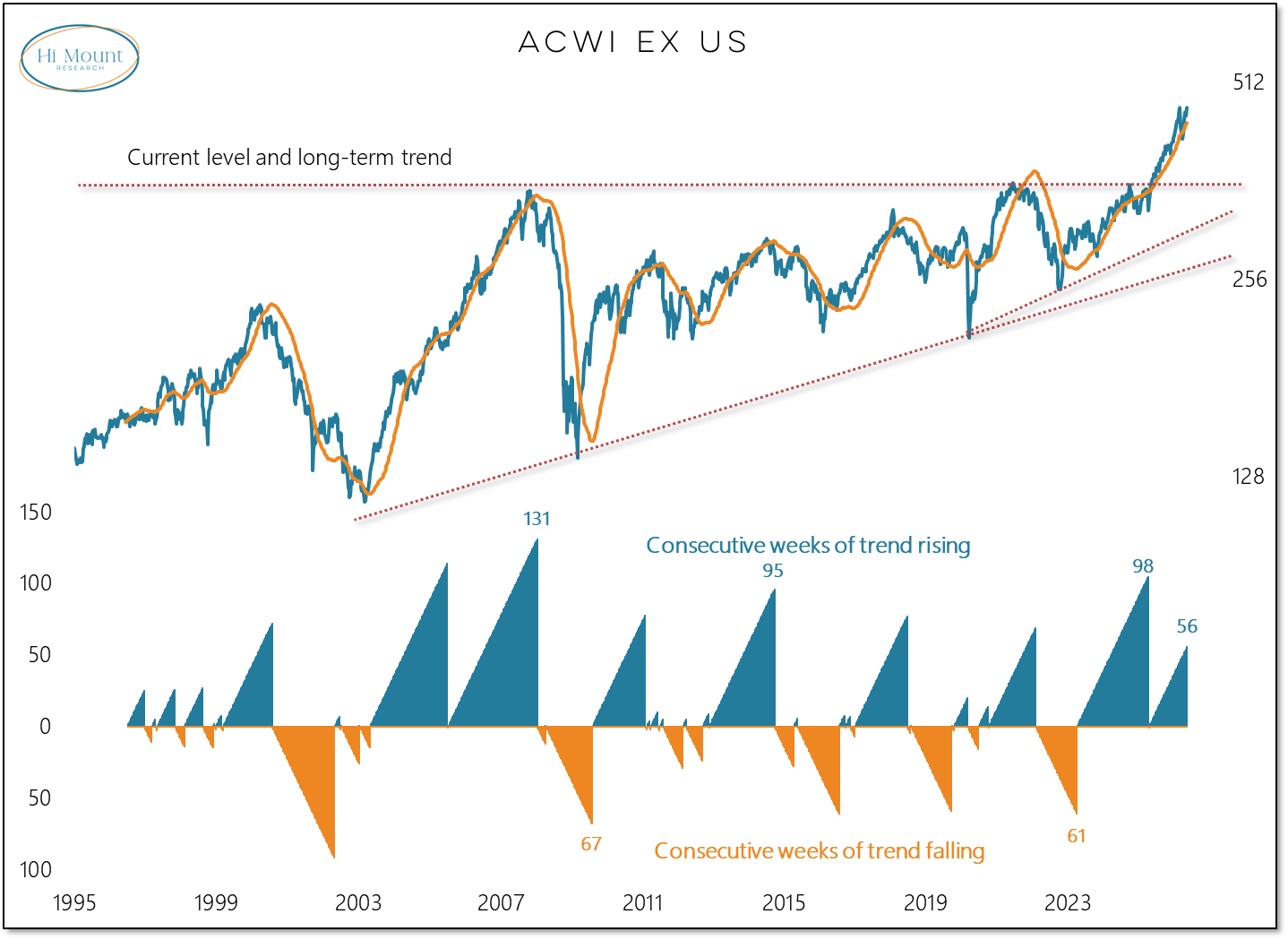

The absence of a breadth thrust during this ongoing rally (which we discussed last week) remains a potentially limiting factor. Poor breadth shows up on a global basis as well. The breadth breakdown in the ACWI trend components was more pronounced than the index itself, and the recovery has been more muted than the recovery in the index (which has already returned to record territory).

While global breadth is out of gear right now, zooming out shows a favorable long-term backdrop for global equities. The ACWI ex US has a rising long-term trend and is just a year removed from breaking out of a decade+ secular bear market with no upside progress. The bulls definitely get the benefit of the doubt here.

Other evidence supporting a bull perspective for now includes evidence of an improving appetite for risk and a sharp turn higher in earnings expectations.