Bulls On Borrowed Time?

Breadth breakdown is becoming a tactical headwind at a time when the cyclical rally is struggling for support

In last week’s update, we highlighted our global trend indicator as it approached an important support level. This week’s update of that chart shows that it has continued to deteriorate, arguing that we are moving from a “return on capital” environment to a “return of capital” environment. Managing risk by moving to the sidelines is a well-tested approach to capital preservation.

{kind=link}

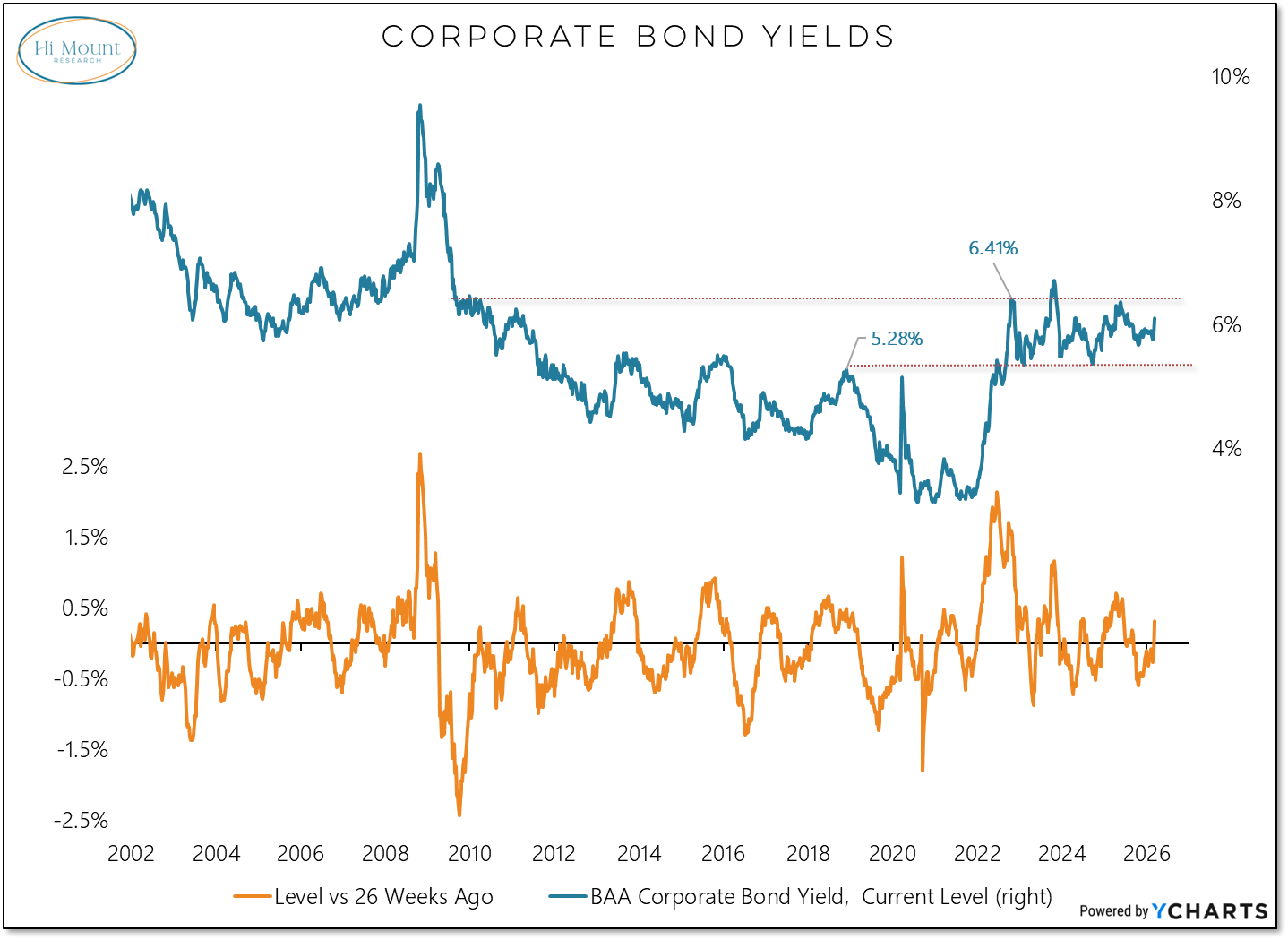

In addition to the Breadth breakdown that continued last week (which we discuss in more detail below), we also observed a sharp move higher on bond yields that is creating a liquidity headwind for stocks (as the 26-week change has moved from negative to positive). Between breadth breaking down and yields pushing higher, next week’s update of the Weight of the Evidence is likely to bring a more somber message: in light of recent developments, bull market behavior is no longer being rewarded.

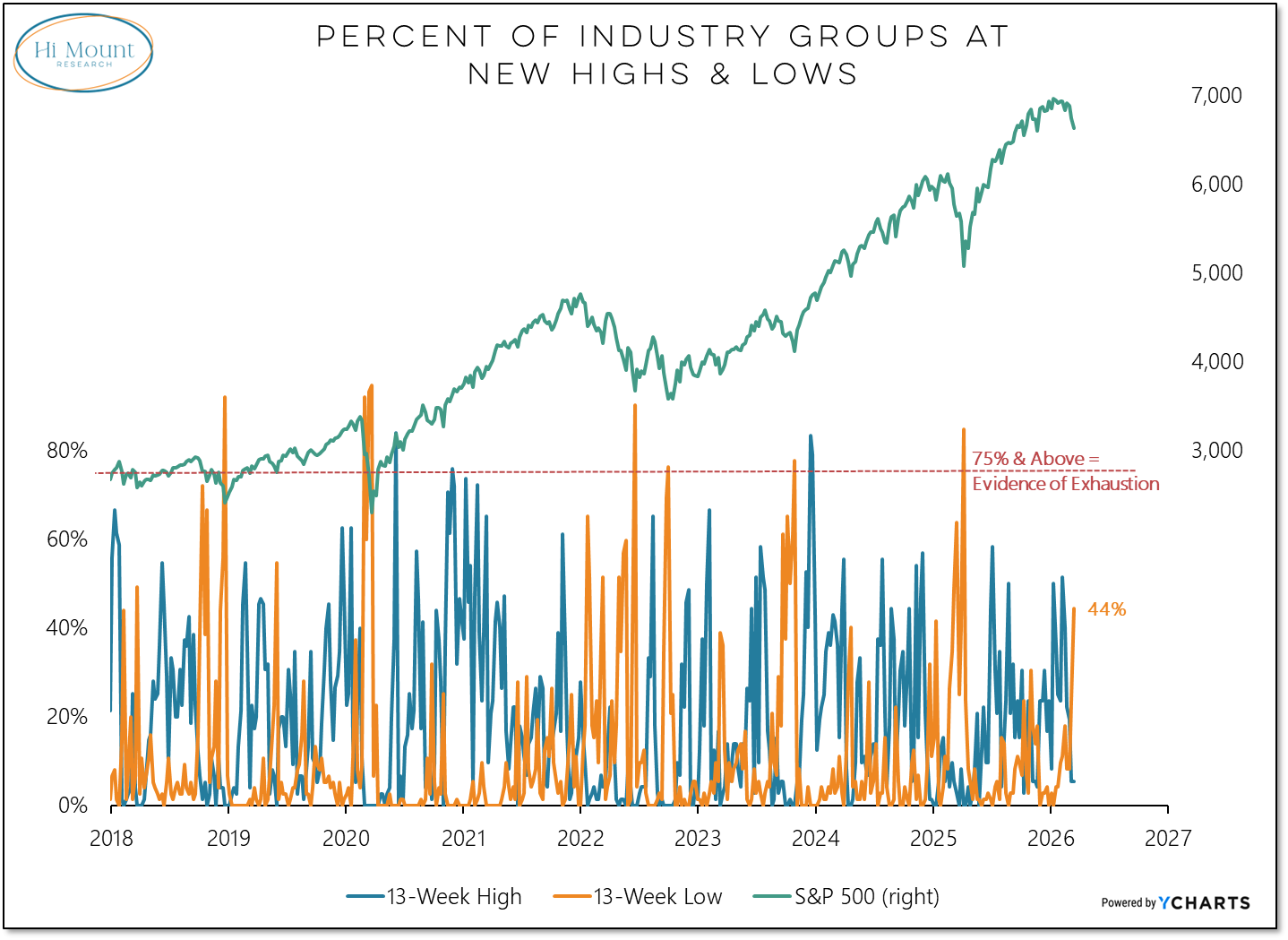

Before getting into the implications of seeing more stocks make new lows than new highs and the looming expiration of last year’s Breadth Thrust Regime, it may be useful to think about the difference between broad market deterioration and evidence of exhaustion. For example, we have seen an expansion in the percentage of industry groups at new 13-week lows in recent weeks, but it has not deteriorated to the point of signaling that selling has become exhausted. In other words, stocks may bounce, but the buyability of that bounce remains in question.

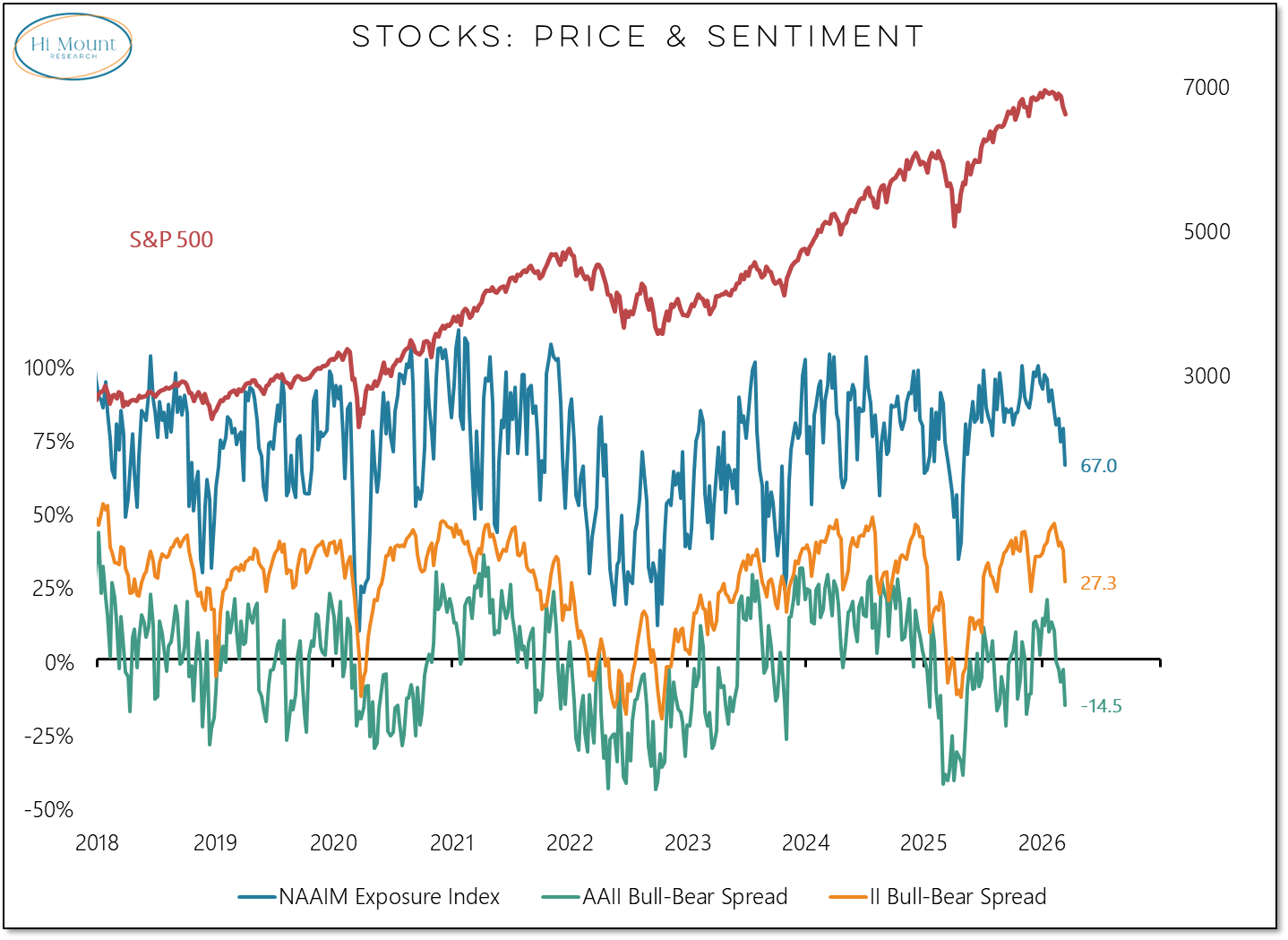

We could add to this analysis evidence that bulls are just now in the early stages of heading for the exits. Sentiment is deteriorating but nowhere near washed out. Talk of sustainable lows appears premature at this point.

{kind=link}