Key takeaway: New highs in new highs as the indexes quietly climb higher support strength into 2025.

The percentage of industry groups in the S&P 1500 hitting new highs last week reached its highest level since mid-2021. Stocks don’t tend to run into trouble when rally participation is expanding.

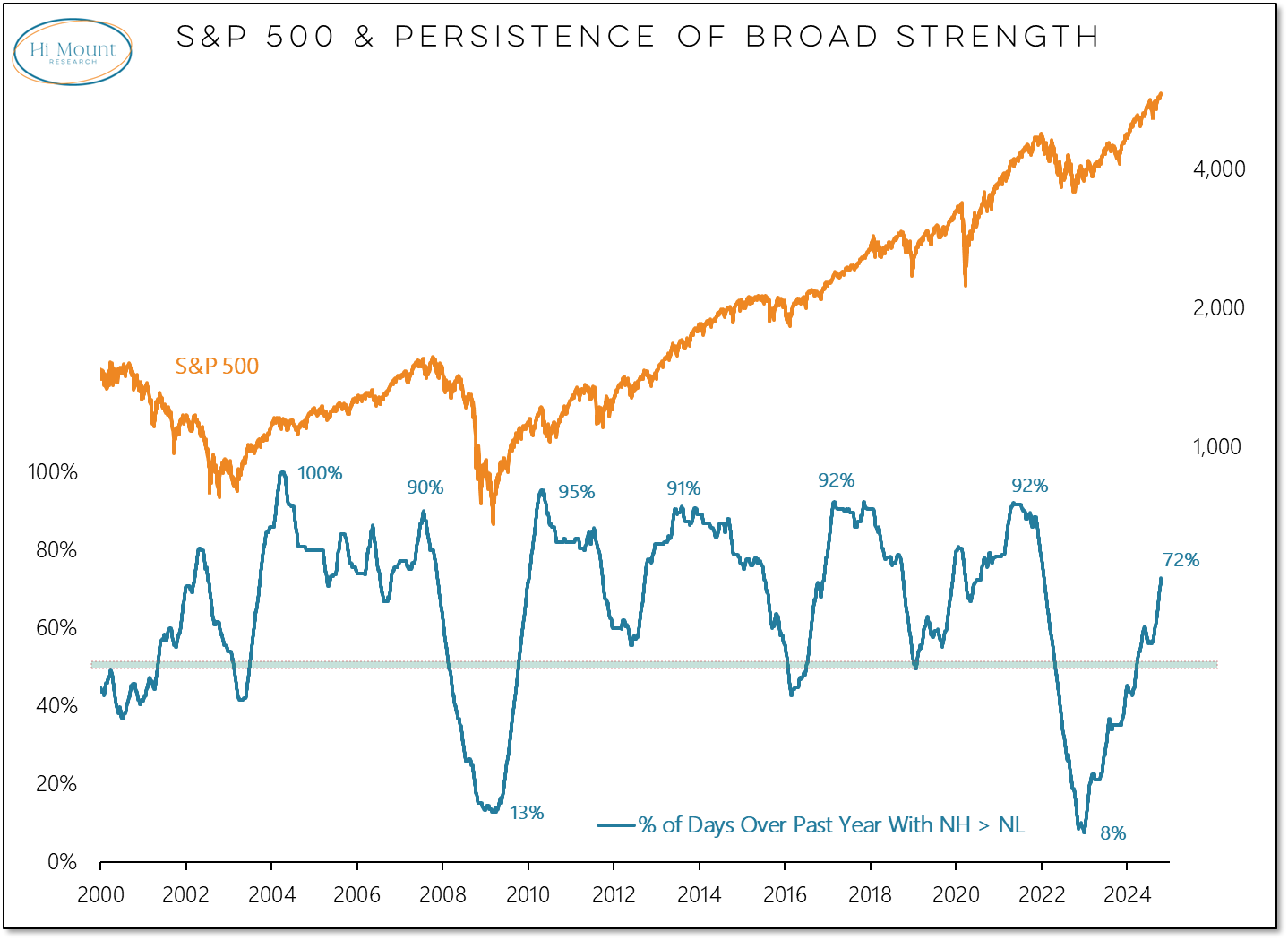

Over the past year, new highs have outnumbered new lows on 72% of the trading days. This has been expanding but still does not look stretched. It is not uncommon to see this climb above 90%.

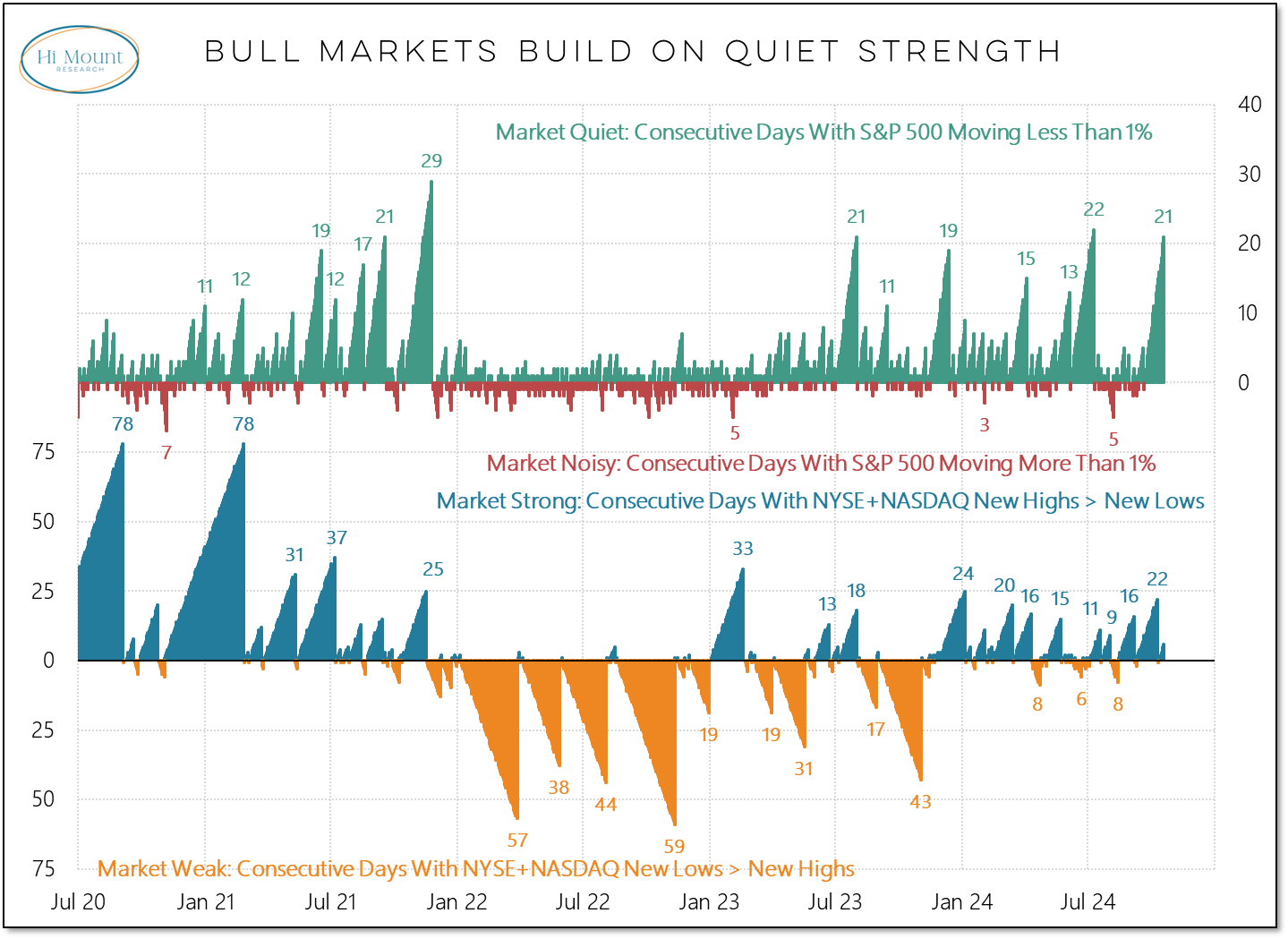

Broad market strength has been accompanied by relative quiet at the index level. It has been 21 days since the last 1% swing on the S&P 500, which is tied for the second longest stretch of quiet in the past 3+ years.

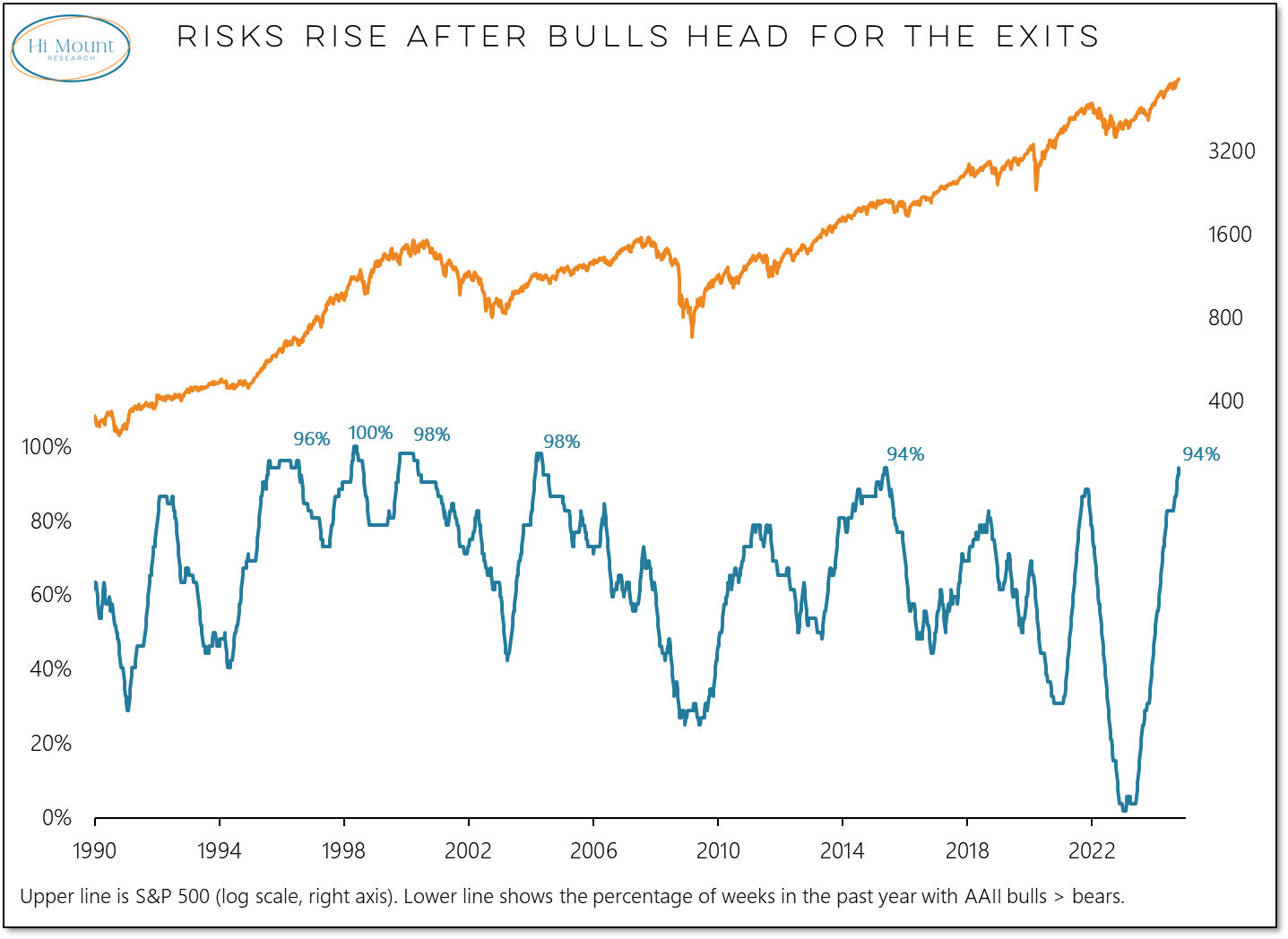

Sentiment right now is a problem for the bears. The weekly surveys shows that optimism is elevated and persistent. Risks rise after the bulls head for the exits.

In summary, the weight of the evidence is tilted away from risk and toward opportunity.

Valuations are still on the risk side of the scales. This remains a longer-term headwind for equities.

New regimes have come and gone over the past four decades. The negative relationship between valuations and forward stocks market returns has been persistent. At 21x, the forward P/E ratio for the S&P 500 is consistent with no not gains over the coming decade.

More details on the weight of the evidence (and what to do about it) are below:

Keep reading with a 7-day free trial

Subscribe to Hi Mount Research to keep reading this post and get 7 days of free access to the full post archives.